As I work with people getting into the self-storage business and use some benchmark terms we use in our business and commercial real estate, I realize that not everyone really understands what the terms really mean.

For example, CAP rates. I have done a couple of episodes explaining CAP rates and what they really mean and don’t mean. If you want to learn more about CAP rates, click here.

But today, I want to talk about two main return metrics that seem straightforward at first glance but are not always really understood.

Cash on cash and Internal Rate of Return (IRR).

I am going to use a proforma in Excel that I recently completed to demonstrate how they are calculated. I am using Excel instead of the Storage World Analyzer because the Analyzer calculates them automatically, and you don’t get to see exactly what goes into those numbers.

Cash-on-Cash Return

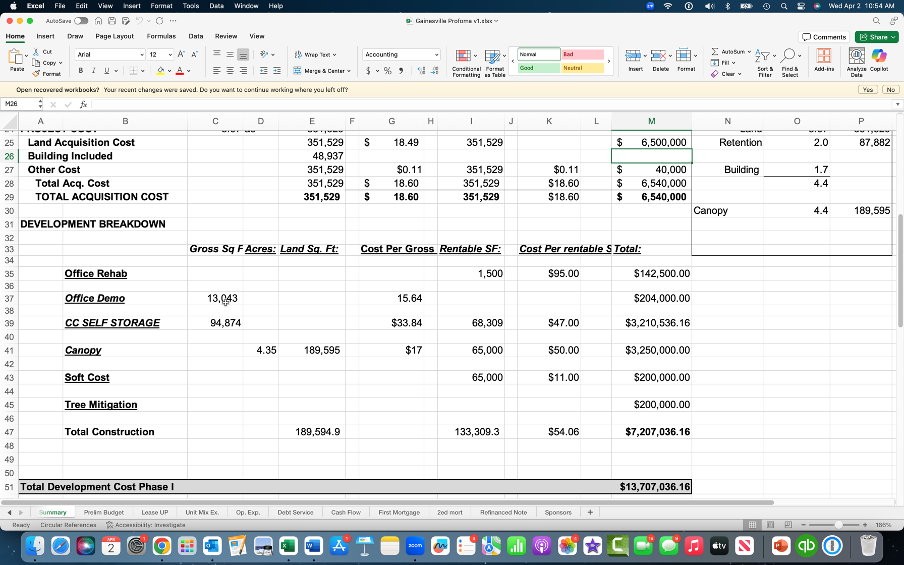

Here is a self-storage conversion and boat & RV development of some additional land.

So, It looks like a $13.7 million project.

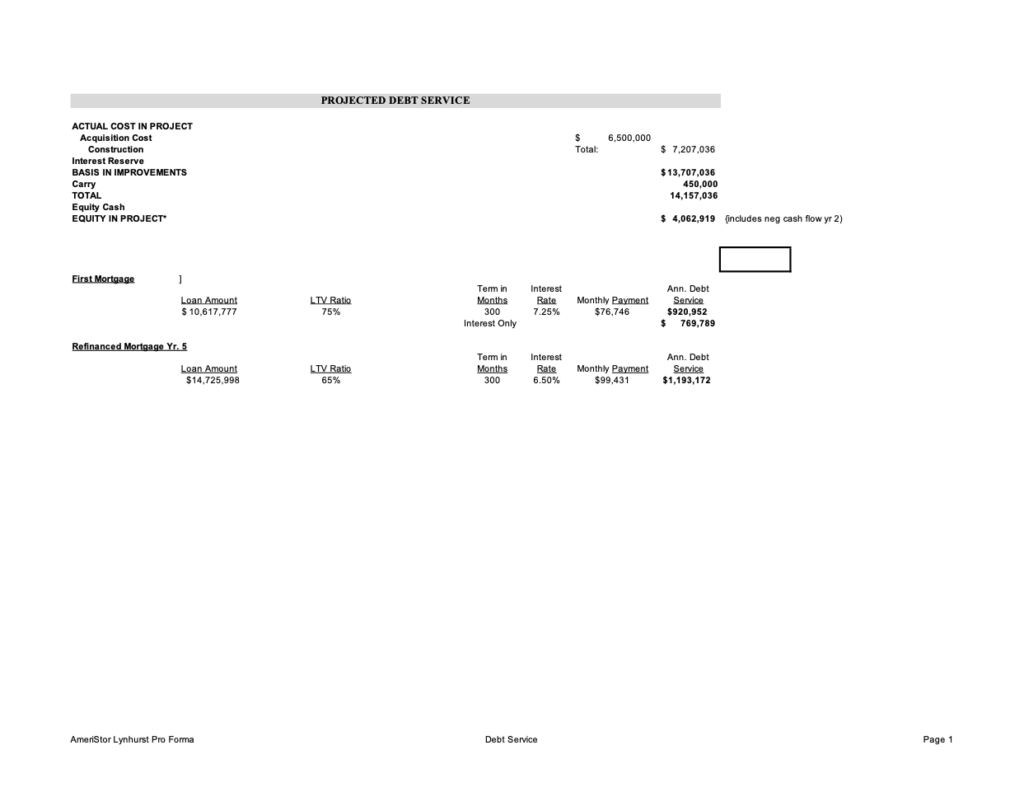

So, if we can get a 75% loan-to-value loan, with some negative cash flow in year 1 included, it looks like we would need to inject about $4,062,919 into the deal.

Now, it does not matter if it is your money or investor money; the “capital stack “on this deal is $4,062,919 cash and $10,617,777 debt.

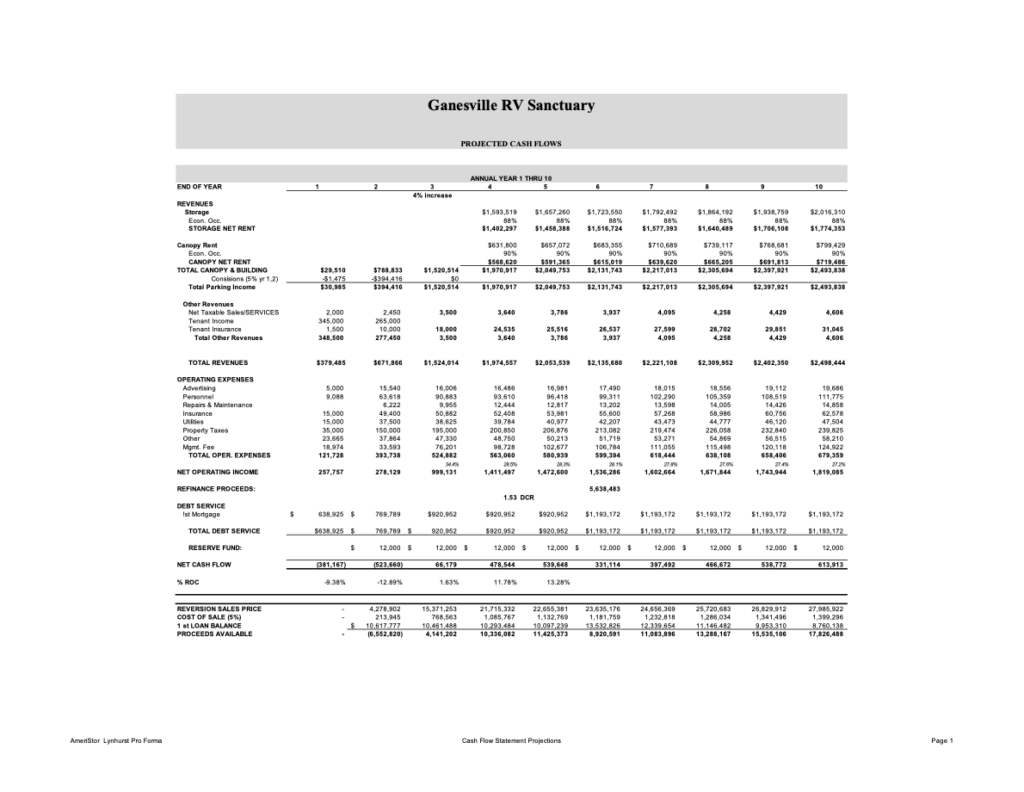

Here is the ten-year projected cash flow statement.

As you can see, in years 1 and 2, there is projected negative cash flow. Then, in years 3 through 5, positive. Then, in year 6, a “liquidity event,” in other words, a cash-out refinance, and then positive cash flow through year 10.

At the bottom of each year is a line called “%ROC.” Return on cash or a cash-on-cash return.

Of what?

Of the $4,062,919 cash injection. The math is in year 3, for example, $66,179 divided by $4,062,919. In other words, in year 3, the $4,062,919 cash earned 1.63%. In year 5, $4,062,919 was earned by 13.28%.

You will notice that after year 5, there is no return on cash calculation because the deal has no cash. We got our initial investment money back from the refinance proceeds.

A simple but important return metric.

So, if you are looking at this deal, the first year stabilized, your money in the deal is earning close to 12% cash-on-cash return.

Is that a good use of your money?

There are other metrics as well like the deal cost is around $14 million with negative cash flow, and at a 6.5% CAP rate, the deal has a value of over $21 million when stabilized, but for this episode, we are focused on the cash-on-cash metric.

For some people, that is a great use of their money; for others, not so much. That is your call.

Cash-on-cash is a critical metric that is not too hard to understand. Now, let’s move on to IRR, where there seems to be a lot of misunderstanding.

Internal Rate of Return

The IRR was designed as a return metric that would allow investors to compare different types of investments with each other and see which deal over the life of the investment generated a better return on the capital.

You could compare oil rig investments to apartments to see which was a better use of the investment money. You could look at two different storage deals that require two different investment amounts to see which generates a better return over the life of the investment.

You should know this for yourself if you are using your own money. However, it is absolutely critical to understand if you have investors or partners.

In the Storage World Analyzer, this is calculated for you and listed at the bottom of the summary page.

However, so you understand, let’s use this ten-year cash flow statement to calculate the potential IRR of this deal.

To calculate an IRR, you look at cash in the deal and cash out of the deal in the different time periods. Given this is a ten-year statement, we are going to create a ten-year IRR.

Let’s put the time periods and the cash flows in a table.

We always start with time period 0. That is when the deal starts, and it usually is a negative number representing cash going into the deal. In this case -$4,062,919. In this table, the time periods are in years and on the left. Cash in or out of the deal is on the right.

|

0 |

-$4,062,919 |

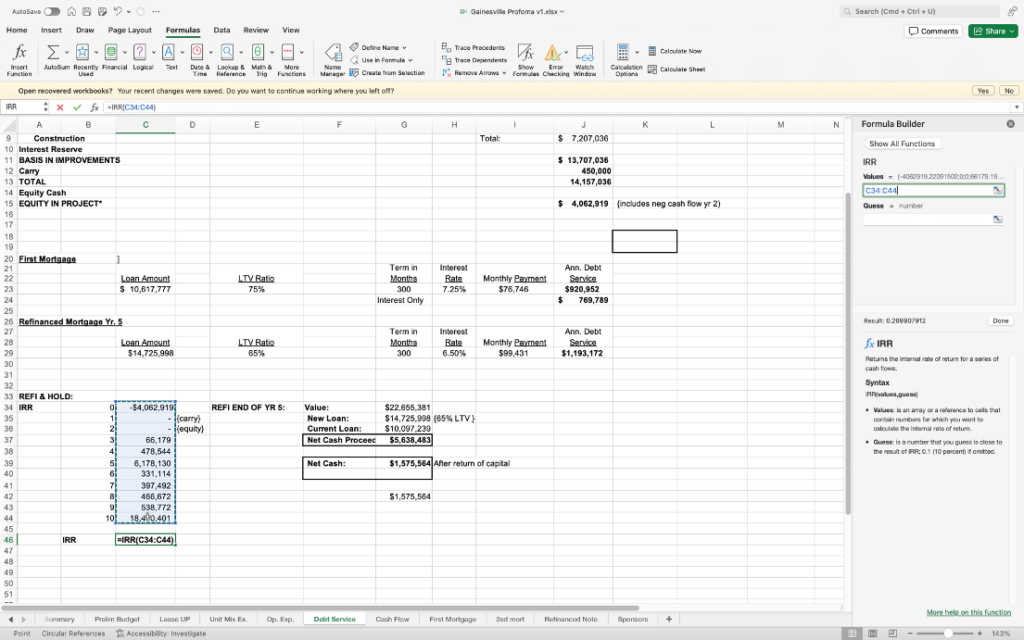

There is negative cash flow in years 1 and 2. If we put the money in in years 1 and 2 as they occurred, I would add them as negative numbers in time periods 1 and 2. However, year 1’s negative was calculated in the loan amount as “reserve” on the debt service page (see above), and the negative cash flow in year two was raised in the cash in the deal in time period 0. So, in calculating the IRR, there will be no cash in or out of the deal in years 1 and 2.

Below is where we are at this point.

| 0 | -$4,062,919 | |

| 1 | 0 – | {carry} |

| 2 | 0- | {equity} |

|

|

Now, in years 3 and four, there is positive net cash flow after operating expenses, loan payments, and reserve funds, $66,179 in year 3 and $478,544 in year 4.

Here is where we are on our IRR table looks like so far.

| 0 | -$4,062,919 | |

| 1 | – | {carry} |

| 2 | – | {equity} |

| 3 | 66,179 | |

| 4 | 478,544 |

Year 5 is a big year for this deal. We are going to refinance the deal. Below is chart showing the projected refinance calculations.

| Value: | $22,655,381 | ||

| New Loan: | $14,725,998 | {65% LTV } | |

| Current Loan: | $10,097,239 | ||

| Net Cash Proceeds: | $5,638,483 | ||

Estimated value at a 6.5% CAP is $22,655,381. It is contemplated that a new, 65% loan to value, the non-recourse loan would go into place, and the existing first mortgage would be paid off. After the existing loan is paid, which leaves an additional amount of cash, we will have the remaining $5,638,483.

It is contemplated for this financial model that the refinance happens in the last month of year 5 or time period 5 for the IRR calculation.

From the ten-year cash flow statement, we can also see that we are projecting a net cash flow from operations in the amount of $539,648, plus the refinance proceeds of $5,638,483 for a total amount of cash out of the deal that year of $6,178,130.

Here is the table so far:

| 0 | -$4,062,919 | |

| 1 | – | {carry} |

| 2 | – | {equity} |

| 3 | 66,179 | |

| 4 | 478,544 | |

| 5 | 6,178,130 |

A new loan is in place, and there will be more debt service over the next five years, but we are still positive. As we add those cash flows in the appropriate time periods, our table looks like this:

| 0 | -$4,062,919 | |

| 1 | – | {carry} |

| 2 | – | {equity} |

| 3 | 66,179 | |

| 4 | 478,544 | |

| 5 | 6,178,130 | |

| 6 | 331,114 | |

| 7 | 397,492 | |

| 8 | 466,672 | |

| 9 | 538,772 |

Now let’s calculate the final year and look at what this table actually tells us.

Every IRR calculation has a start period and an end period. The end period almost always has a sale. Even if we were not really going to sell in year 10, we would have to calculate the net sales proceeds to get an accurate IRR projection.

Now, this is a “before tax” IRR calculation.

Mostly, that is what is used in the industry today because most of our projects are set up in LLC formations. The tax implications flow straight through each partner and investor in the form of a K-1. Each member of the LLC has a unique tax rate and situation.

However, if it is just you, you could calculate your “after-tax IRR” if you wanted to.

So, for year 10 in this financial model, we see there is a projected $613,913 in positive cash flow from operations and a projected $17,826,488 net sales proceeds from the sale (disposition) of the asset.

Our table is now complete and looks like this:

| 0 | -$4,062,919 | |

| 1 | – | {carry} |

| 2 | – | {equity} |

| 3 | 66,179 | |

| 4 | 478,544 | |

| 5 | 6,178,130 | |

| 6 | 331,114 | |

| 7 | 397,492 | |

| 8 | 466,672 | |

| 9 | 538,772 | |

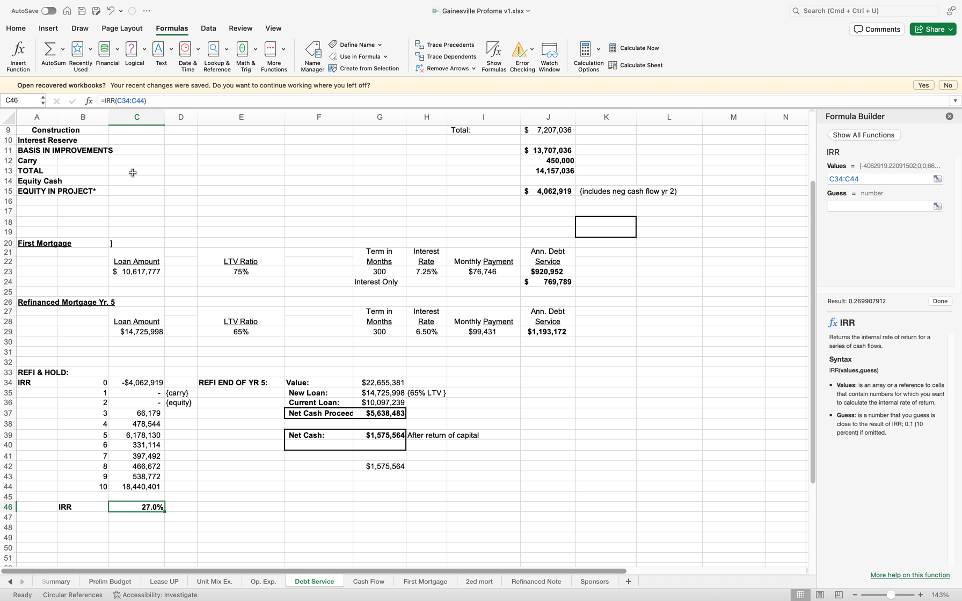

| 10 | 18,440,401 |

So, what will this table tell me?

If these are indeed the cash flows of this project, what this table will tell me is what the initial investment of $4,062,919 averaged as a return in this investment per year over the life of the investment.

This way, I could compare this deal to another storage deal, apartment deal, or any investment to see what a better use of my money.

Also, one could look at the risk potential of the deal. If most of the cash flows, for example, are scheduled toward the end of the time period, there is more risk.

In this deal, we had the negative cash flows accounted for (reduced risk), a liquidity event in year 5 (again less risk), and positive cash flows from year 3 through the end of the deal.

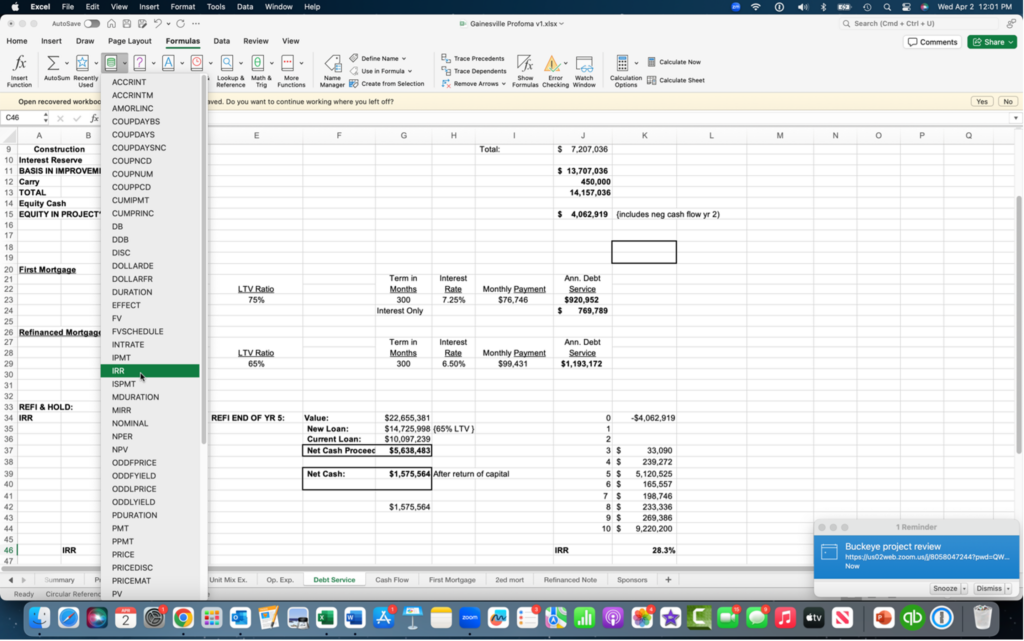

So, what will the initial investment be projected to earn per year over this deal? Let’s see how to calculate that number in Excel.

What we do is go to “Formulas” on the Excel page, click “Financial,” then go down the formulas to “IRR.”

Then, you highlight the cash flows from time period 0- to time period 10. On the right of the screen, you click “done,” and presto, you have your IRR.

So, in this deal, it is projected the initial investment of $4,062,919 will average a 27% return per year for the life of the deal.

Would you do that deal? Is that a good average yearly return on your capital?

This was a quick way to actually see how the two main financial metrics of investment real estate and, specifically, self-storage are calculated and what they really mean.

For example, I had at one time a minimum of 12% cash on cash return when stabilized, and a minimum of a 20% IRR on a ten-year cash flow statement as my minimum metrics for a deal. Those were just mine. I am not saying they should be yours.

I hope this helps as you go out and analyze deals and go forth in this great business of self-storage.