Some dots have connected in my mind recently that are reshaping how I evaluate self-storage trade areas moving forward. Surprisingly, this insight came from digging into the lives and current work of the people who shorted subprime financial instruments during the Great Recession—and what they’re focused on today.

As a CCIM in the commercial real estate space, our state chapter recently hosted Michael Litt to speak on the “Big Short.” If you remember the 2015 movie by the same name, it gave a dramatized (but abbreviated) version of what his hedge fund did during the 2008 recession. After that event, I started researching Litt’s work—and what I found not only fascinated me, but also directly impacts how I’m planning and investing in self-storage today.

A Brief Look Back: The Big Short of 2006–2008

Litt was an asset allocation manager in the FrontPoint Financial Strategies Fund, an equity long/short hedge fund. Around 2006, he wrote a research paper entitled “The Great Compression” that highlighted how fundamentals in the credit market had become disconnected from credit pricing due to the leverage embedded in structured credit products. He was one of the first—if not the first—to see the looming crisis and helped fund a new hedge fund designed to short this market.

In this week’s episode, we’ll focus on the administration’s tariff policies, how they may affect the economy, and what we’re focusing on in self-storage. Next week, I’ll dive into the One Big Beautiful Bill Act (OBBBA)—what’s in it, what’s likely to happen, and how it may reshape both the storage space and the broader economy.

To get a general overview of Litt’s take on where we are at this moment in time—and to set the backdrop for these two episodes—here are a few bullet points:

- The economy and jobs are weakening slightly, and inflation is now showing up in price data.

- He projects a .25 basis point interest rate reduction in the last half of 2025.

- OBBBA has significant economic stimulus components over the next four years.

- However, OBBBA will add $3 to $3.5 trillion in national debt through 2035.

- The tariffs function as a consumption tax of between $200 billion and $300 billion annually.

- Uncertainty tends to delay economic decisions (I can confirm this firsthand in fundraising).

Today, let’s focus on tariffs and how I’m using that information to evaluate trade areas.

As we speak, tariffs are already in place, and more are being added. Canada, for example, has a “35% tariff,” but many items are either excluded or taxed at a lower rate. Mexico’s overall tariff rate is lower than Canada’s. It’s challenging to piece together the true effective tariff, but from what I can gather, it’s roughly 18% on imports—and it’s expected to increase.

To much of the world, these tariffs appear to have no consistent logic. A 50% tariff on Brazil because of their prosecution of a former president the administration favors? A 35% tariff on Canada but not on Mexico because of differences in how the governments speak to—and about—the administration? The firing of the Labor Statistics Chief because numbers were revised to a figure Trump didn’t like?

Not to get political, but the reality is that much of the rest of the world views this as petty and unstable. Many institutional investors and foreign governments believe tariffs are being used to punish those the administration dislikes and reward those who approach it with “respect.”

We’ll get into this more in the next issue, but a valid question is: why should we care what any other country thinks?

Well… here’s why.

At any given moment, as much as two-thirds of long-term U.S. debt is purchased by foreign investors—both private and governmental. They’ve been drawn to long-term U.S. Treasury Notes because of their safety, security, liquidity, and the overall reliability of the U.S. economy and its treasuries.

But that picture is rapidly changing in the eyes of the rest of the world. This means fewer buyers and/or higher returns being demanded (i.e., higher interest rates to fund U.S. long-term debt) due to the growing perception of instability in our economic policies and economy.

It doesn’t matter whether that perception is “true” or not—perception is truth—and money flows either to where returns are highest or where it feels safest.

More on this next week.

For now, let’s look at the tariffs.

How Tariffs May Affect Storage Demand

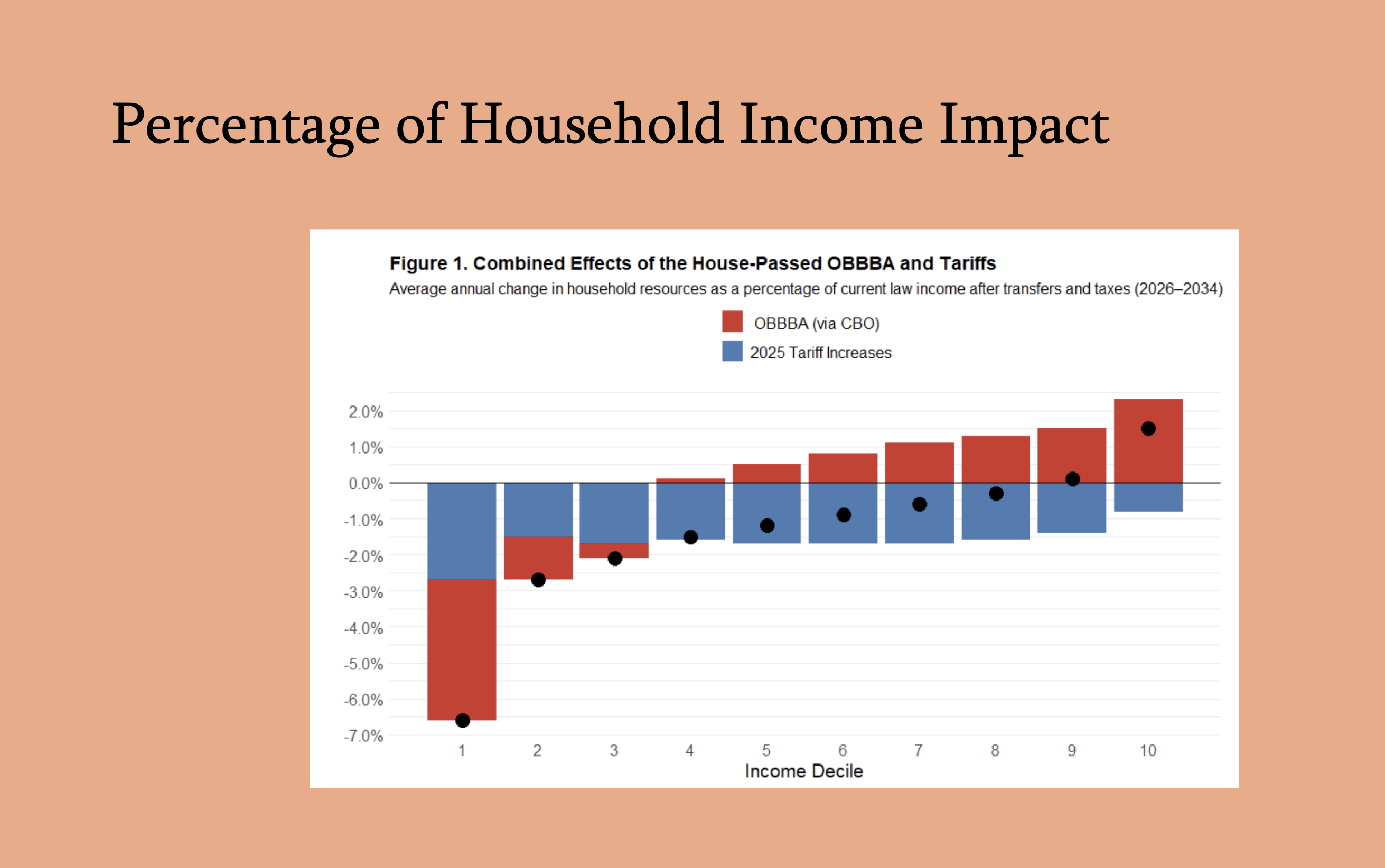

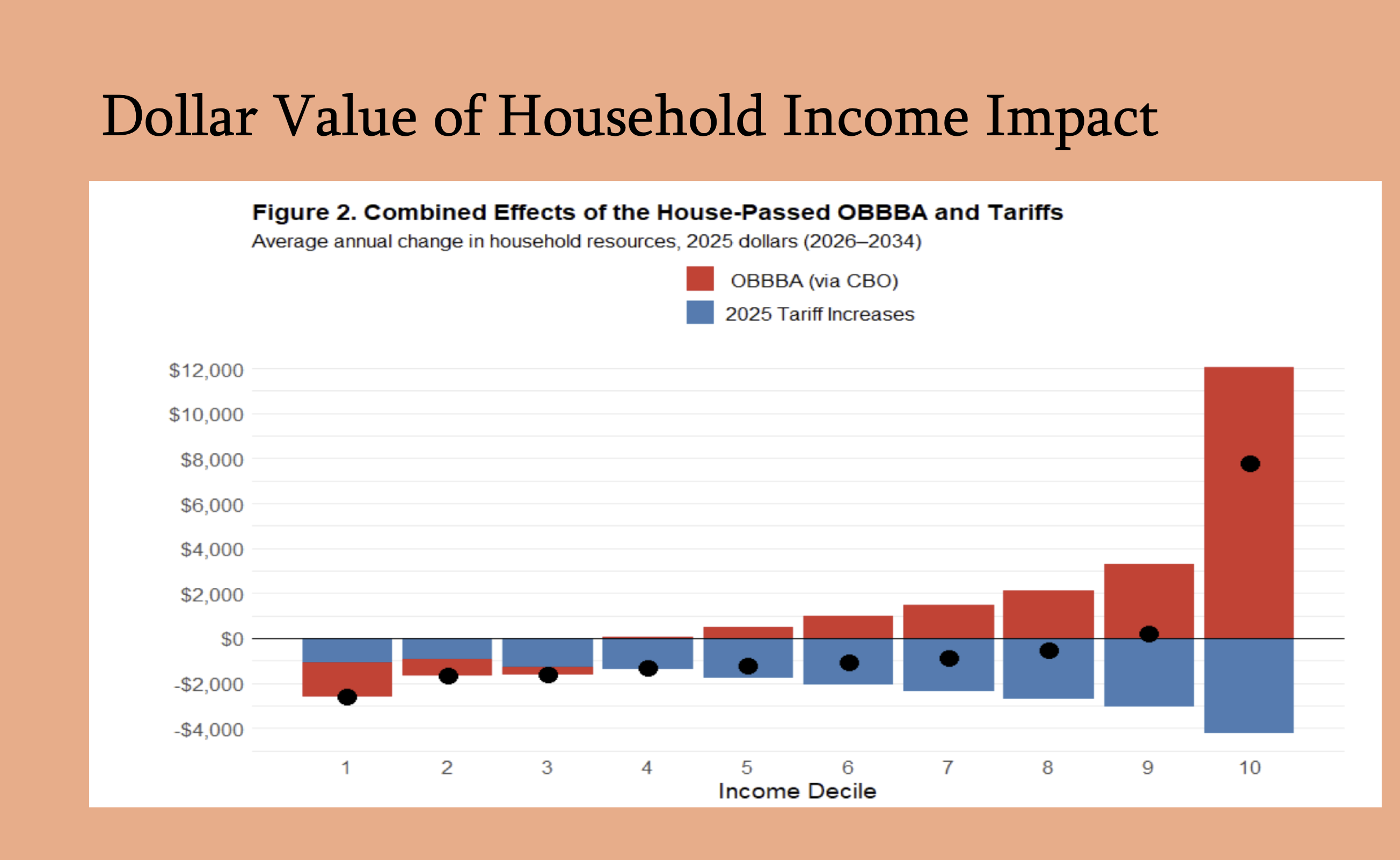

Litt breaks down how tariffs and OBBBA impact American households by income decile (i.e., dividing the U.S. population into 10% slices from lowest to highest income). The charts he shares show that (1 on these charts is the lowest income and 10 is the highest).

This is the type of analysis Litt does to figure out where he is going to invest his funds resources in the upcoming years, and given his track record, I tend to put way more credence in this than anyone from Washington I have listened to in the past 20 years or so.

Let’s just focus on the blue or tariffs. Here is how Litt sees them affecting the household resources as an annual change by percentage, and below by average dollars.

Now I doubt if many in deciles 1 or 2 rent much self-storage. But in deciles 3 through 5 or 6, the consumption tax effect of the tariffs could have quite an impact on discretionary spending.

- The lower-income deciles (1–5 or 6) are most impacted by tariff-induced loss of spending power.

- My experience aligns with this: customers in those deciles have shorter stays in storage.

- Shorter stays = lower customer lifetime value = higher churn = higher marketing costs.

- If you’re in lease-up, you may end up leasing the same unit 2–3 times before stabilization.

- That extends the lease-up timeline and cuts into your interest-only period, a nightmare if amortization kicks in before you’re cash-flow positive.

Therefore, more than ever, we are looking at trade areas that not only have higher rent structures to combat the higher interest rates and construction costs, but I am also now focused on higher-than-before median incomes in the trade area.

How do we determine that?

A Tool We’re Using to Measure Income Stability

Offering Memorandums (OMs) only tell part of the story. Median income by zip code, city, or county is helpful, but it’s too generalized.

Let me show you a fairly new feature in a subscription service that I and the people in our Inner Circle are using. Perhaps many other subscription services that focus on storage space offer this feature. I’m just not sure.

Now it may look like I am selling or have an affiliate relationship with Radius Plus, but I don’t. I get nothing, and I hope theyare okay with me sharing this. If you are interested in learning more, search for Google Radius Plus and contact Alex directly. He has been very helpful to us in the Inner Circle.

Let me walk you through how we’re applying it. Here are some real deals I am doing and looking at.

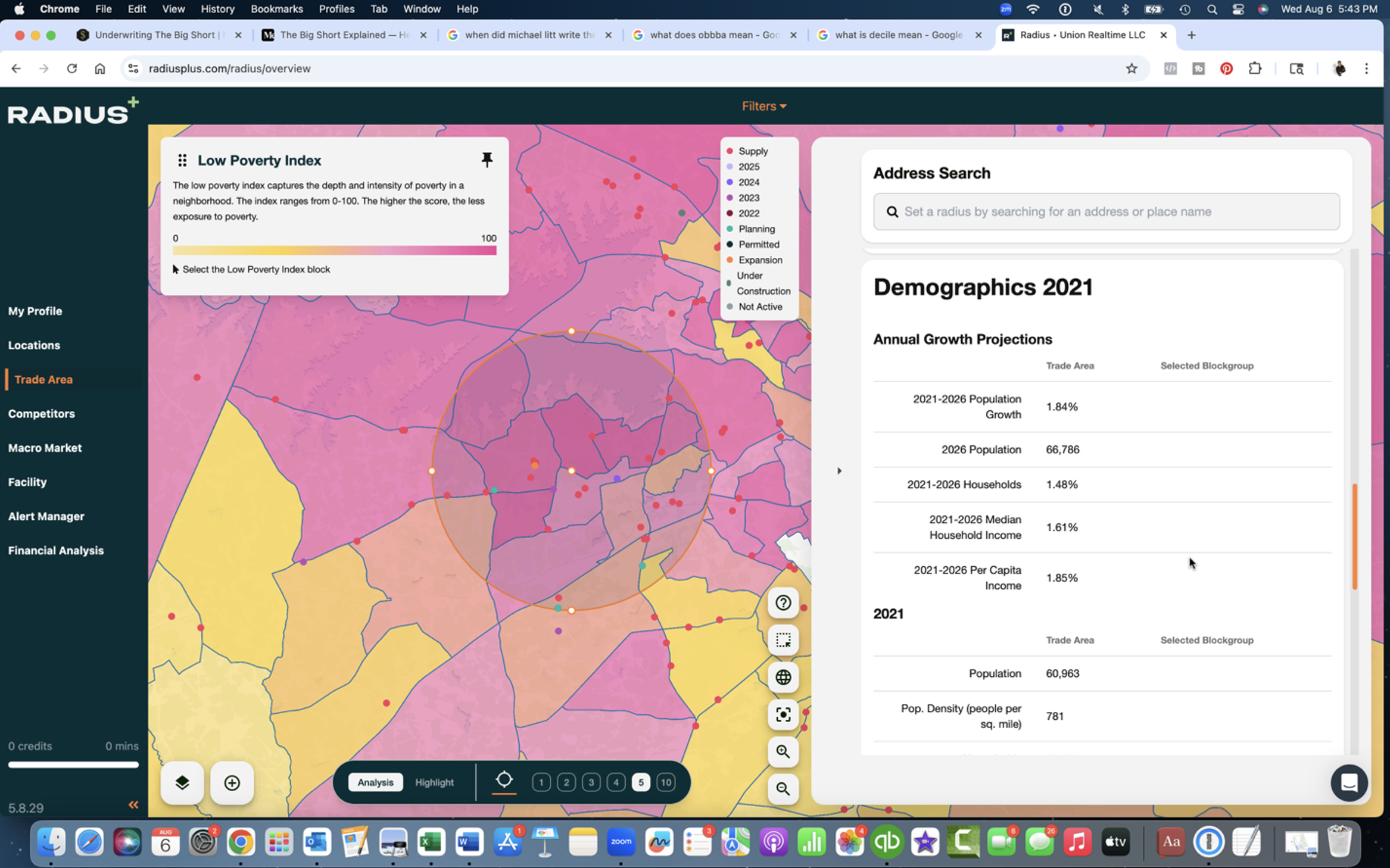

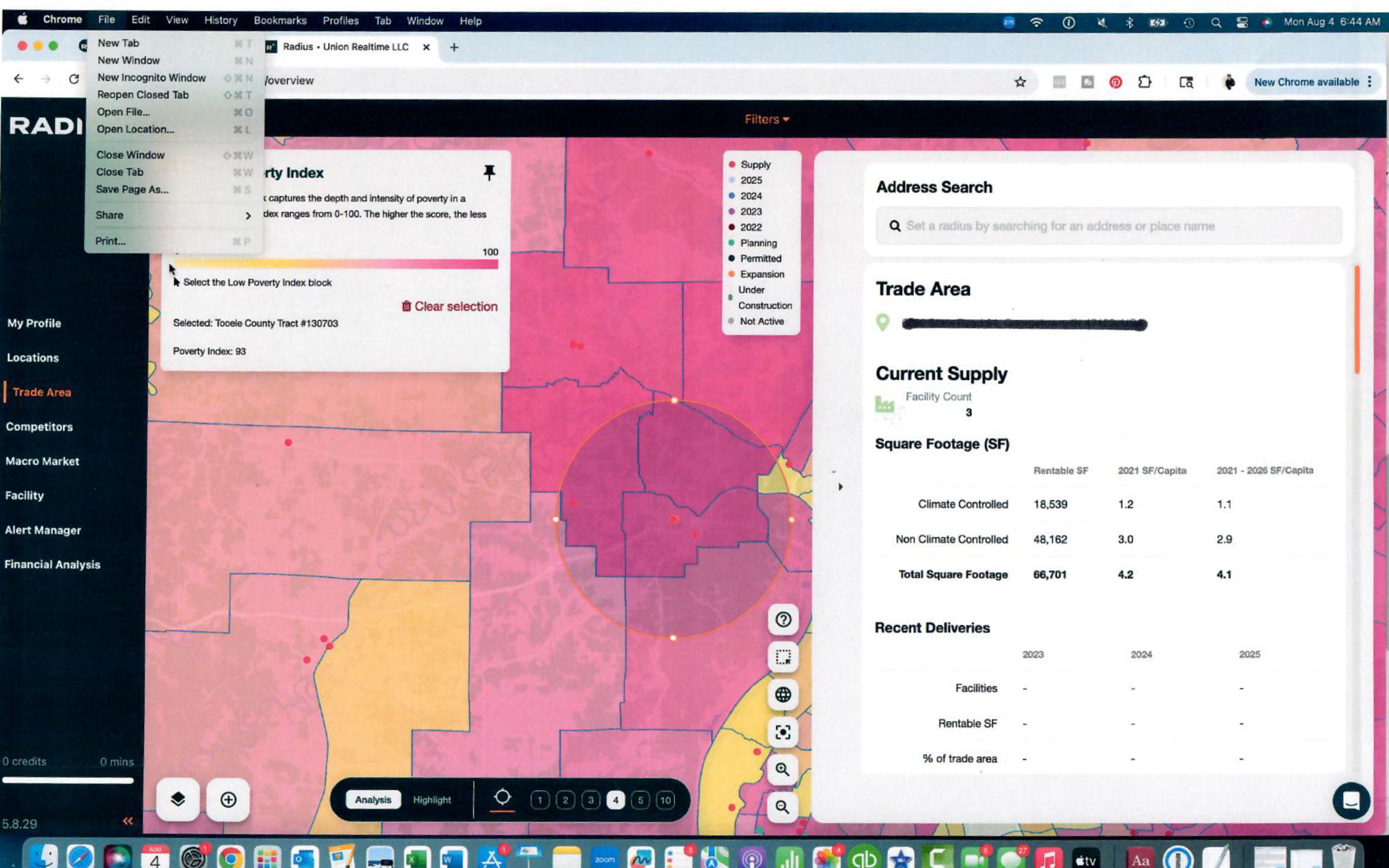

First, there is a location for a large Boat, RV, and self-storage project construction is starting on. There is a feature one can click on called “Low Poverty Index.” I am not sure why it isn’t called “Wealth Index,” but I didn’t name it.

In this Index, you can see that most of the trade area is in the upper third of the income index block. We feel safe moving forward in this trade area and feel the consumption tax effect of the tariffs on this trade area will be less impactful on us.

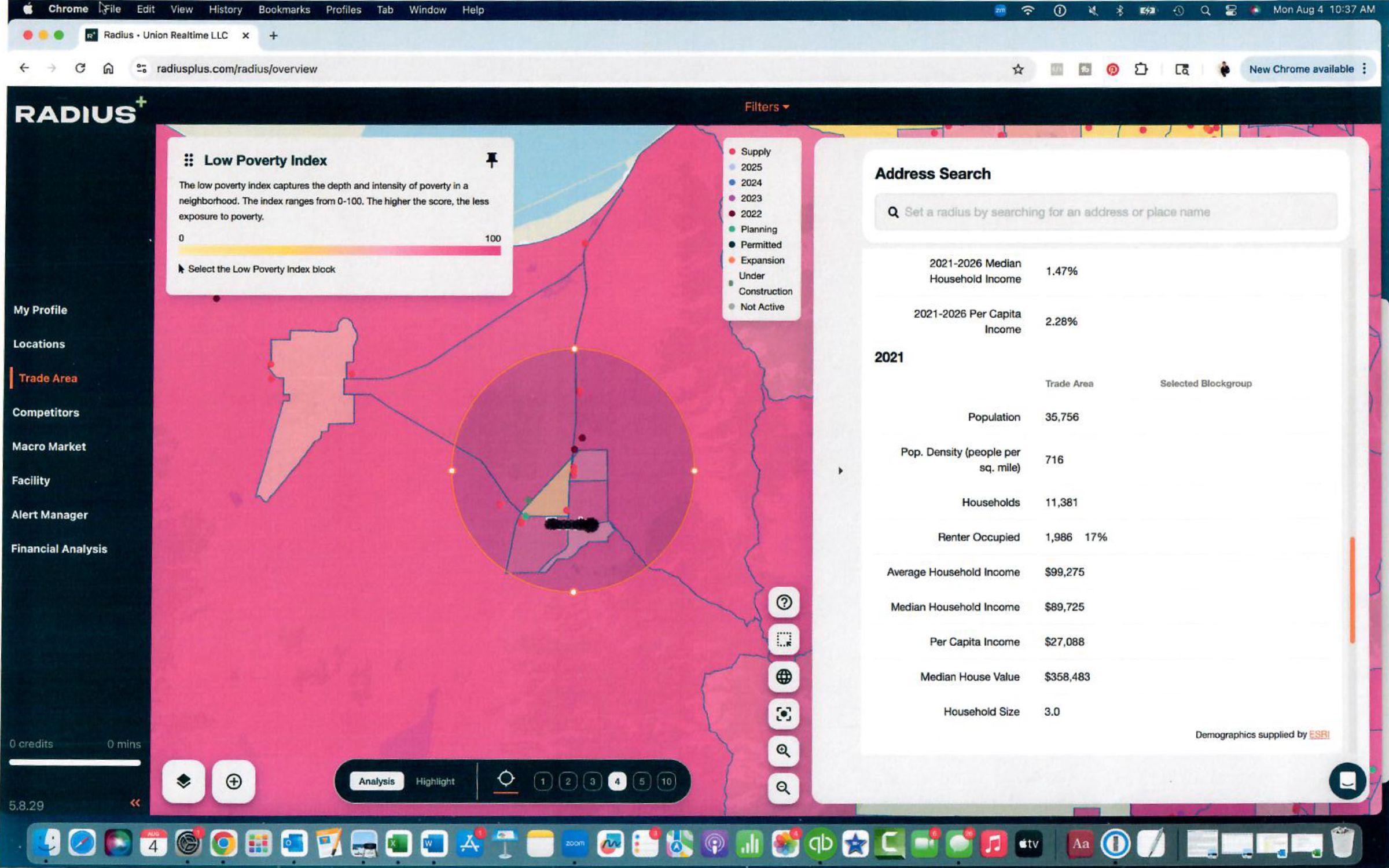

Once I began to see what Litt is hedging on (I’ll share more next week), I quickly pulled this feature up on another project we are doing. It is an expansion. Here is the location with the Low Poverty Index overlayed.

Again, what I expected because of our initial research, but it felt good to have it confirmed. The yellow is a business/industrial block with no residential homes in it.

Finally, here is a location in a smaller market we are writing an LOI on.

In my opinion, it has never been more important to make absolutely certain—not just that the rates are there and the demand is there—but that you’re positioned in roughly the upper third of the income index for the foreseeable future.

As you can see, even in smaller markets, this rule can still apply, as with the one we’re currently considering writing on.

Final Thoughts

Next week, we’ll go over more of the details of the OBBBA that was recently passed—how it affects you as a property owner, the positives, the potential pitfalls, and its impact on both the short-term and long-term economy.

As always, I’m learning out loud. I’m simply sharing what I’m seeing, researching, and applying to my own business strategy. I’m not trying to change anyone’s political views.

Well… maybe a little.