Last week, we started a conversation about what I’m seeing in the economy, what may be coming next, and how that changes our self-storage strategy, based on research I dug into after hearing Michael Litt speak. As a CCIM in commercial real estate, our state chapter hosted Litt on “The Big Short.” If you remember the 2015 movie by the same name, it dramatized (and abbreviated) what his hedge fund did during the 2008 recession.

Litt was one of the first, if not the first, to spot the looming crisis years ahead by doing the hard research on where to place capital. His fund earned north of 500% during the Great Recession. When I noticed people coming in from all over the eastern US to hear him, I started studying his work. What I found not only fascinated me; it directly affects how I’m planning and investing in self-storage today.

One of my biggest takeaways: follow the money. Capital flows where asset allocators believe the best risk-adjusted returns are, not where the headlines or politicians point. From my research, very few anticipated and profited the way Litt’s fund did.

In Part 1, we dug into Litt’s 2008 maneuvers, today’s tariff regime, and how we’re adjusting trade-area analysis. (Here’s the link to last week’s episode.) Today, we’ll unpack the OBBBA, the recently passed tax bill, look at likely impacts across income levels, the broader economy, and how this shapes our self-storage tactics. I’ll also share what it looks like Litt is long and short today, based on his public commentary and research.

Quick note: I put far more weight on this kind of research than on news or party talking points. Call it capitalism in its most basic form, no ideology, just probabilities and expected returns.

What’s In The OBBBA (and what matters for storage)

(Bullet points summarized from Litt’s review of the bill’s provisions.)

1) Immediate expensing of domestic R&D (Sec. 174), retroactive to 2022

This doesn’t really impact us in the storage business or commercial real estate industry, except as it may relate to our tenants, who are most likely larger corporations where R&D is a vital part of their business.

The bigger picture: a lot of private-sector R&D happens in partnership with universities. Those programs have seen significant defunding this year, which could dampen private R&D going forward. Because the provision is retroactive, firms can benefit immediately from money already spent.

2) 100% expensing of Owner-Occupied Qualified Production Property (QPP)

- New factory/plant construction, first use by the taxpayer

- Must be integral to manufacturing, refining, or agriculture (initially chemicals & ag

- Construction must begin Jan 20, 2025 – Dec 31, 2028 (yes, that 1/20/25 date again)

- No Office, Administrative, Sales, or R&D Components Qualify.

3) 100% Bonus Depreciation

- Nonresidential interior improvements (QIP)

- Short-life assets identified via cost seg

- Storage impact: immediate positive effect on the net cost of capital improvements.

4) Sec. 179 cap raised: $1M → $2.5M

- HVAC, roofs, security & fire systems, doors, insulation, windows

- Storage impact: another near-term net-cost positive for upgrades.

5) Interest deduction rules improved (Sec. 163)

- Switch back to the EBITDA standard increases deductibility

- Many taxpayers can avoid electing out of 163(j) and still keep the bonus on QIP

- Storage impact: more room for interest deductions and depreciation together.

6) REIT & QBI adjustments

- 199A (QBI) made permanent; phase-in raised $75k → $150k

- REITs can hold 25% of assets in taxable subs (up from 20%)

- More generous interest deductions under EBITDA

- Storage impact: not a direct change for smaller owners, but REIT returns may get a tailwind, expect stiffer competition from public and private REITs.

Bottom line on provisions: these can accelerate storage capex projects. Just remember the other side of the ledger: tariffs are inflationary (a consumption tax), and materials/labor costs can rise. Run the net after-tax effect on each project.

The Price Tag: Deficits, Debt, and Confidence

However, these benefits are coming at a cost. The cost is the impact on the national debt over the next ten years.

Let’s look at various think tanks and the estimate of the overall impact of the OBBBA per year. The average of them have the debt increasing from $21 trillion dollars to $53 trillion by 2034.

- The Budget Lab at Yale: $3.5 trillion

- The Congressional Budget Office: $3.4 trillion

- Penn Wharten Budget Model: $3.2 trillion

- Tax Policy Center: $3 trillion

And even the administration’s ally, the Tax Foundation, projects a $1.8 trillion impact from the OBBBA, and that is assuming that the effects of the bill reduces interest rates to 3.25%.

Do you see interest rates dropping to 3.25%? We can begin to understand the reaction of the administration to the Federal Reserve Board chairman more clearly now.

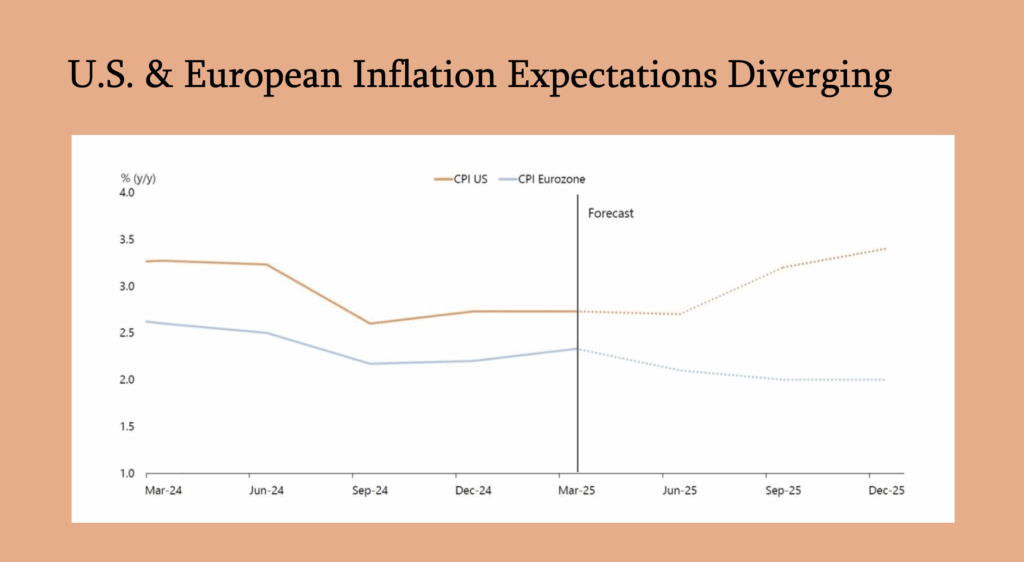

The real issue I see is that the rest of the world sees this as well, and the stability of the US dollar is going to slide downward. If global investors question the stability or credibility of US economic policy/data, they’ll demand higher yields to hold our debt. That compounds the problem.

Cutting SNAP, cutting Medicare, those are a drop in the bucket and in no way address the deficit heading straight to us. At this point, we can’t cut spending in any meaningful manner that begins to fix what is coming.

In a healthy economy, it is fine to have the national debt be around 3% of the GNP (gross national product).

Here’s the trajectory Litt’s research lays out for the deficit as a % of GDP over the next decade:.

Currently, prior to OBBBA: 6.1% debt to GNP

OBBBA as written: 6.8% debt to GNP

OBBA permanent: 7.8 debt to GNP

Lower confidence in the dollar follows naturally from higher, sustained deficits plus tariff-driven inflation.

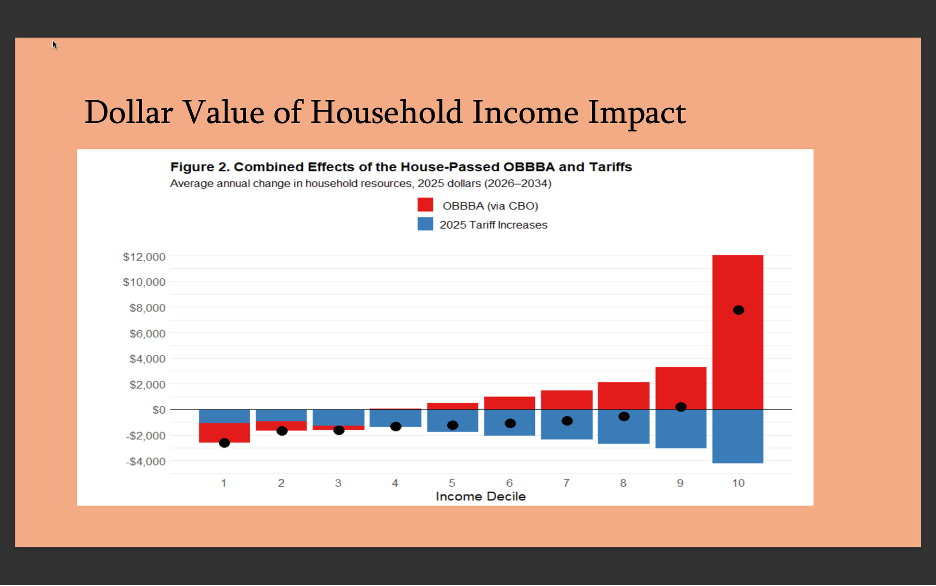

And if you remember the chart from last week, as we discussed the tariffs, let’s now look at it again with the OBBBA in.

Tariffs and OBBBA by Income Decile

Litt breaks down effects by income deciles (1 = lowest 10%, 10 = highest 10%). Tariffs act like a consumption tax, touching all deciles, while OBBBA’s benefits are concentrated at the upper end.

If you remember, the tariffs function as a consumption tax and will affect all income deciles. And as we can see, the OBBA will have a positive impact mostly on the upper end of the income distribution as well.

Now, a fair argument I have heard is that the tariffs and the revised tax bill should promote more US production and factories, and more employment.

Well, let’s think this through.

Yes, additional plants and manufacturing facilities may be built. Let’s take computer chips. The administration is using 100% (again, extreme) tariffs for computer chip imports. So let’s say Apple builds a domestic chip manufacturing facility.

What we have seen in the past decade is that, even though US manufacturing is down, productivity has dramatically increased due to robotics and automation. How many people will really be hired?

In Kentucky, a new Ford plant was announced for EV production. It will employ 2,200 people. About half are engineers. In the past, there would have been thousands working on production lines. Today, there will be hundreds managing robotics lines and working on the lines themselves.

This is what manufacturing looks like today and in the future.

While tariffs sound emotionally appealing to the blue-collar population of the US, which helped put this administration into office, in reality, they will most likely see the least positive impact from the tariffs and the OBBA.

Hence, our shift in what we are focused on in self-storage trade areas as described in last week’s episode.

Let’s look at what I can see as his investment strategy moving forward from here.

What Litt’s Fund Betting On

1) Short U.S. Dollar

- Tariff-driven inflation and larger, persistent deficits under OBBBA

- Policy instability (e.g., firing data chiefs when numbers are unfavorable)

- Global confidence risk in U.S. economic policy credibility

If foreign buyers step back, the U.S. must offer higher yields, which worsens the fiscal math.

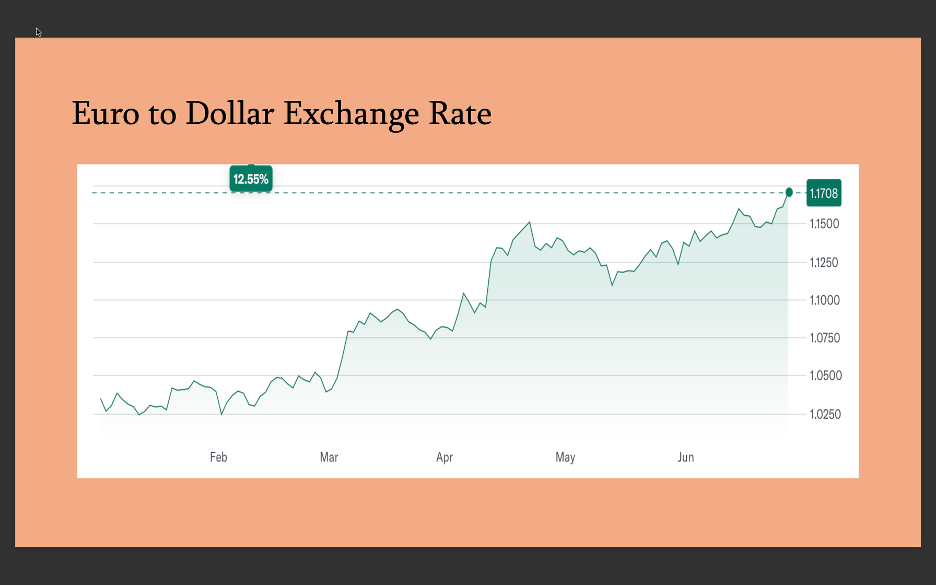

So where will investment most likely go? From what I can tell, he is thinking of Europe.

Europe and the Euro.

Long in Euros.

It looks like long in the Euro currency.

As capital looks for relative stability, the Eurozone may attract flows. The directional view appears to be long EUR / short USD.

What We’re Doing in Self-Storage

- Trade-Area Targeting: We’re concentrating on higher levels of income in trade areas (roughly the 65th–100th percentiles) where tariff-driven inflation (consumption tax) bites less and discretionary budgets support steady demand.

- Capex Timing: We’re green-lighting improvements where OBBBA provisions (QIP bonus, Sec. 179, interest deductibility) materially improve after-tax returns net of expected cost inflation.

- REIT Competition: We expect more aggressive REIT competition in the future. We may focus on projects and areas that REITs are not focused on.

- Selective International Exposure: I’m exploring passive allocations to European storage where the macro backdrop may be more stable. I’m not moving or developing there, but as we harvest profits from U.S. projects, I’ll look at certain European markets alongside U.S. opportunities. If you’re interested in pooling capital for passive European self-storage exposure, let me know.

This does not mean we’re stopping U.S. development, conversions, or expansions. We’re tightening criteria and being more surgical about where and when we build or buy.

Conclusion

I am sharing my research as I evolve my thinking and strategies in the self-storage business. I put more confidence in research like Litt’s because there is no ideology or political view to move forward. He is looking for where the profits can be made based on what is happening.

Don’t take what I am writing and just run with it. Do your own research and come up with your own idea of what is happening. Don’t take the news, a politician’s, or a political party’s version of what will happen and run with it. Do your own research. It has never been easier.

Think for yourself and, based on what’s happening, with as little as this right or wrong or good or bad as possible (very hard for me), make your decisions now as to what to do based on what you see happening in the future.

This is our job as entrepreneurs and self-storage owners.