“You can never lose money if you’re selling your self storage facility for a profit.”

At least that is what I’m telling myself.

We recently received an offer from a REIT on some of our self storage expansion projects and the value is what we projected in year 10, not this year.

We are not in the market to sell, but sometimes the Universe has different plans.

I have talked to a number of you with the same issue. You did a value-add project…the project is stabilized…and you get unsolicited offers at very high values.

You have to decide whether to sell now or wait and hope it’s worth more in the future.

This is a great problem to have. In my book, Creating Wealth Through Self Storage, I said the quality of your life is a function of the quality of your problems.

Want a great life?

Create great problems!

Selling early and making a bigger profit than you expected qualifies as a great problem.

So let me take this opportunity to show you the life cycle of an expansion we did.

A few weeks ago I went through the life cycle of a project from purchase to conversion. In this situation, I’m using the term conversion in the context of paying the investors their investment back and any unpaid preferred return. If you didn’t see or read it, please click HERE.

We were actually starting the process of converting the project that is the subject of this episode when we received the offer. It came in under a 6% CAP rate so we decided to take it. Again, as you will see, it is for about what we projected it would be worth at year ten of the project.

In the summer of 2014 prices were getting very high for existing self storage. I received an email from a Texas broker for a 34,200 square foot project. The physical occupancy rate was listed at 89% and the economic occupancy at 73% (it turned out to be lower than that). The list price was $2,000,000.

The list price was under a 6% CAP rate for the existing income stream. After careful adjustments from the Broker – adding more income and getting the economic occupancy rate up over 12% – the price was then a 7% CAP rate on the asking price.

That usually annoys me because it is my time and my money that gets the income up from where it was and the package indicates I have to pay for that.

There was some obvious deferred maintenance and the project had some parking income.

But I got excited as I often do when I see projects like this.

There was a gap between economic and physical occupancy and land for expansion.

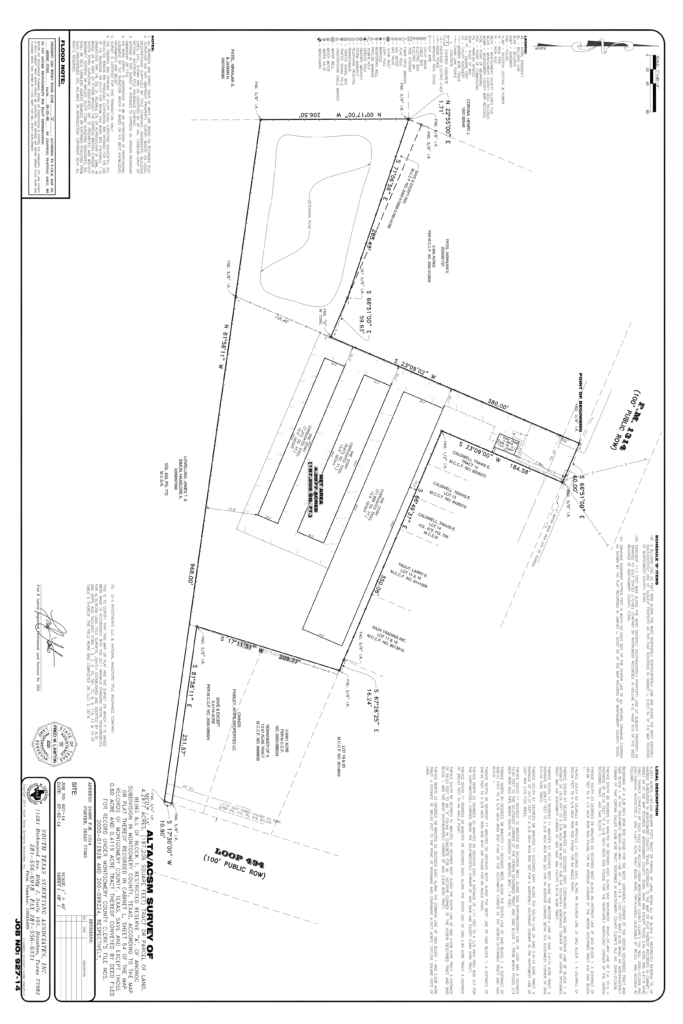

Our business strategy is to put into service projects with a minimum of 50,000 square feet so we can exit by selling to institutional buyers. It was a good thing I went a little deeper into the email. The parking and vacant land included in the listing is what made it meet our criteria for a project. I asked for the existing survey:

I saw the land and got very excited.

This happens often, but my enthusiasm is often dampened after I run a preliminary analysis.

The land available for expansion was a little under 2 acres. That was great. I have discovered we can get about a 33% efficiency on land for projects like this. In other words, an acre is 43,560 square feet. If you multiply that by .33, you will get a good estimate of the net rentable square feet you can build on that acre of land.

I estimated we could get approximately 20,387 more square feet of self storage.

Here was the process I went through:

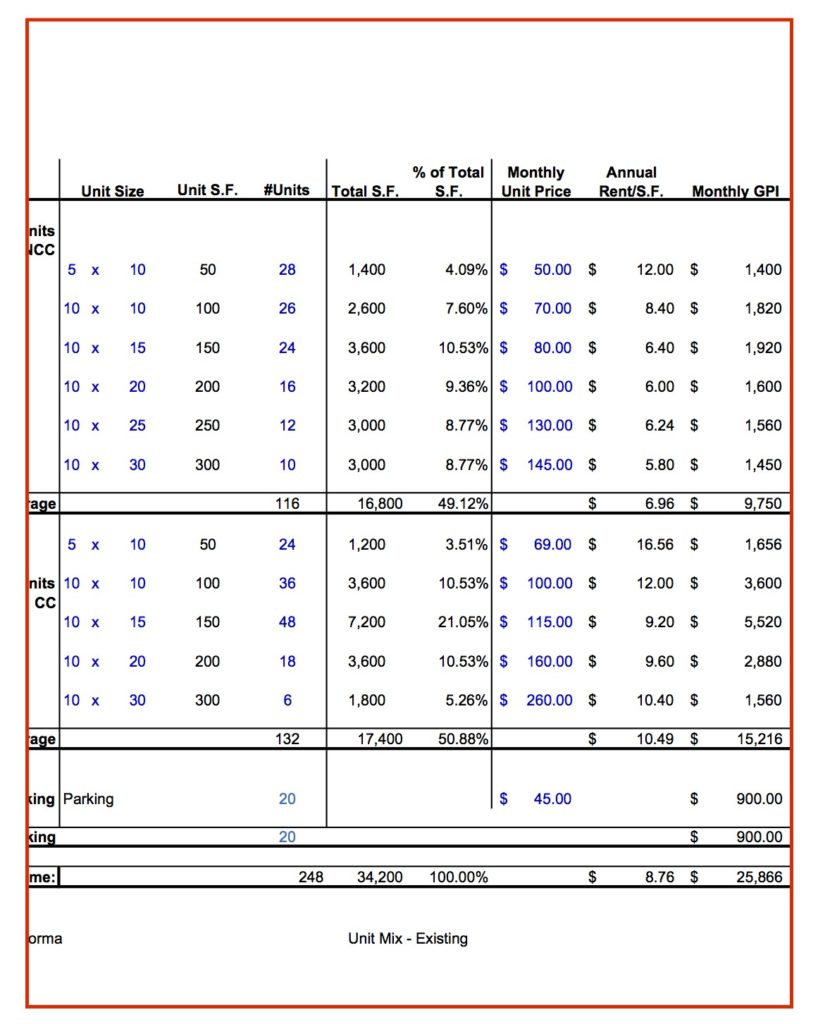

First I took the existing unit mix:

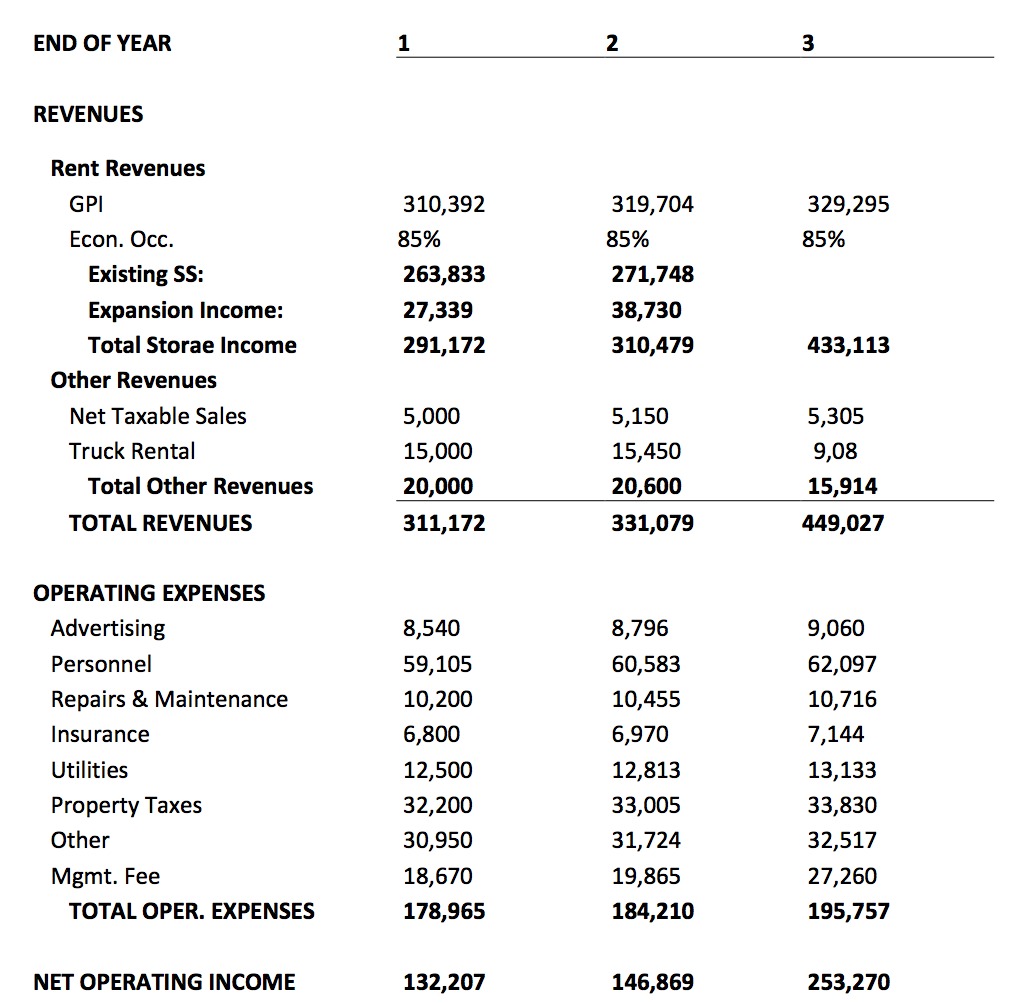

The unit mix spreadsheet above includes the Gross Potential Income (GPI) and the per-square-foot income possible. I used these numbers in my Proforma. I used the GPI and put occupancy at 85%. If we didn’t feel we could get the economic occupancy from the low 70 percentile to at least 85% we wouldn’t purchase.

I also used the psf income in my lease up analysis of the new space.

Next, I entered the operating expenses. Not their current expenses, but what I figured ours would be based on how we run projects. Ours are almost always higher than in the sales packages. This was no exception. The sales package operating expense number was $100,743. My projected first-year expenses were $179,965.

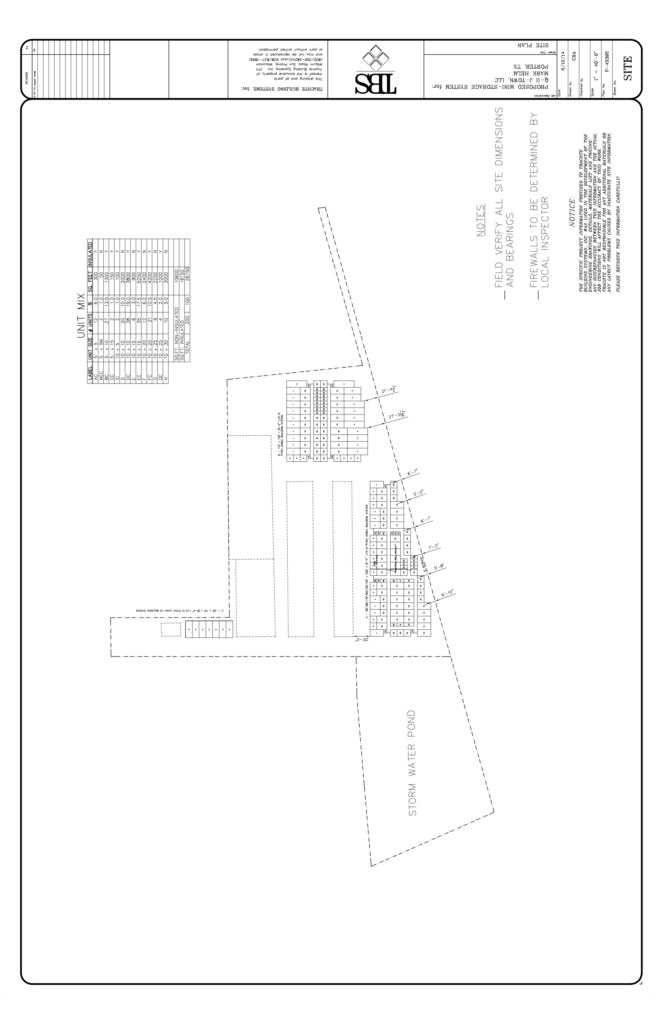

Then I made an estimate of the cost of construction $858,844, which was about $30 psf. It was low. Today our costs are much higher but back then fabrication costs were substantially lower. It turned out that we could actually get 26,750 net rentable square feet based on how we could design the buildings. Our fabricator laid out the plan for us.

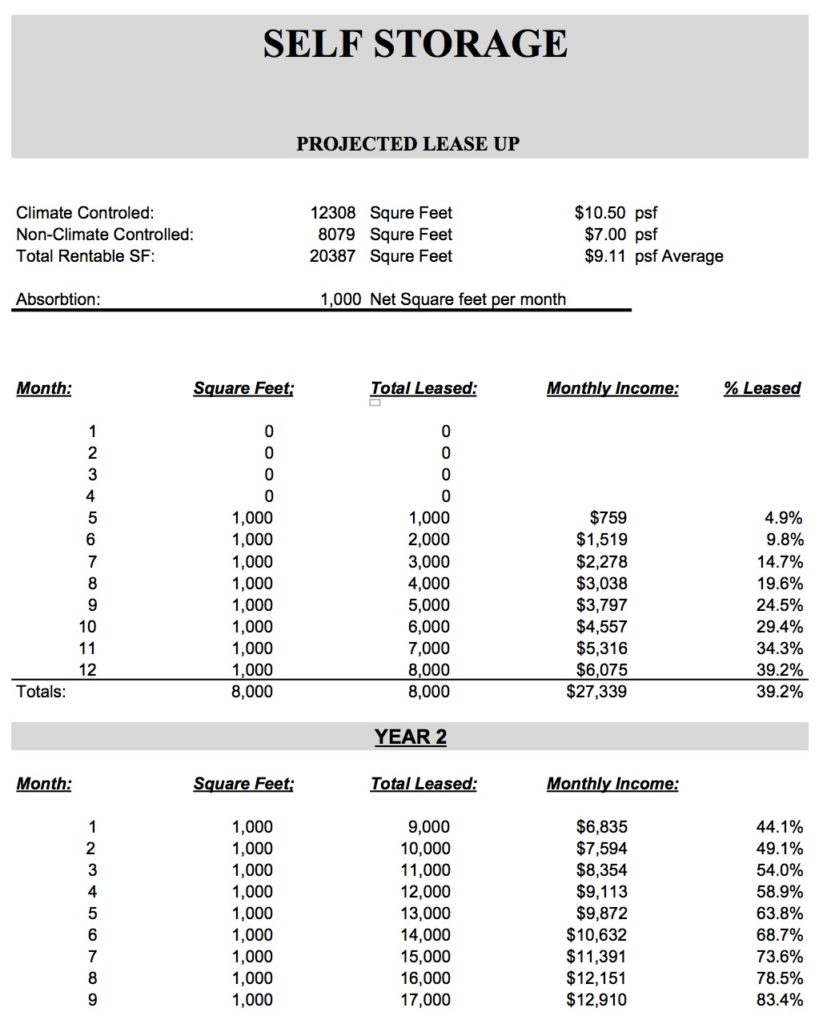

Next, I estimated the lease up. The feasibility report indicated it should be around 1,200 net square feet per month. In my attempt to be conservative, I used only 1,000. This was my biggest miss because the absorption was actually over 3,400 net square feet per month lease up.

All of this together created a project that looked like it could work. Not a killer project, but one that met our business strategy. It looked like I could average over 12% cash on cash return the first five years. And we could refinance at the end of year 5 and get enough to pay our investors back.

I estimated this project would cost us $2,822,844 for the acquisition and construction and would be worth $4,148,036 at the end of year 5.

We put the property under contract at $1,960,000 and started our due diligence. We had to make a few adjustments, but not much. After getting the feasibility report and then the bank loan, we closed in September of 2014.

My first big mistake was the engineer I selected.

We just didn’t get along. After 6 months and about $30,000, we fired him and went looking for another.

I learned exactly how important engineers are. Always seek references and make sure you are both on the same page. It is critical your engineer is someone you feel you can work with and has your back. They usually drive the projects through approval and in my experience they can make or break the success of the project.

Then it rained.

And it rained some more. But I was very optimistic. I honestly thought we could start getting income six months after we closed. I told everyone, “…we may not be complete on construction, but I think we can be making some income by then by leasing what we have completed”.

This deal taught me a lesson. It took over a year to get construction completed to the point we could start leasing. Today I always have at least one year for approval and construction time.

When we finally did complete construction we were slightly over budget and we were eleven months behind in income from the new space.

Some banks view this as a problem, some don’t follow it too closely.

The bank we were using did. They were on us constantly and beginning to think they had made a mistake. I kept assuring them things would be fine, we were just behind on construction.

It turned out I was correct. We leased up the new space so fast (again an average of 3,400 net square feet per month), that soon we had caught up with the Proforma.

At the end of the second year of operation, we were over $200,000 in NOI, $51,031 more than on the Proforma for that year.

We were slightly under the next year on the NOI – by about $8,000. Which is funny because that was about the cost of the “Cost Segregation Report” we had completed.

What was also off, however, was the debt service. It doesn’t show it on this form, but our loan payment was about $9,000 higher per year than I originally projected. This represented the overage on the construction. What that affected was the preferred return. We were not paying the full preferred return. Where we were short was accruing and I wasn’t too worried because I knew we would soon be refinancing and paying back any unpaid return.

We had started the financing for the conversion. Our lender told us to wait until the third quarter of that year and then it would be worth $3.7 to $4 million. We could then refinance, pay off the loan (about $1.8 million), and have enough to pay back the initial investment and unpaid preferred returns.

Under our business model that is the point where we, the “common members,” start getting the majority of the cash flow.

Then we received an offer well above the $4 million.

As of this moment, we are a couple of weeks from closing so I am not sure what I should or shouldn’t say, but it was well over $600,000 more than we thought the value would be on the refinance.

So we decided to accept the offer. It was the value we had projected in year ten of the Proforma.

You will be faced with these decisions as you put your self storage into service.

There were times in the process of creating this value-add I was not sure if we were going to come out on top. But we just did the next thing to do and trusted the numbers.

This was one of the first expansions we completed, so it makes sense this would be one of the first we received an offer on. You too will most likely have this “problem” of having to decide to sell earlier than you planned to make a larger profit than you planned.

But remember, the quality of your life is in direct proportion to the quality of your problems. Want a great life? Create a new and interesting problem.

Enjoyed your article, as usual. A couple questions come to mind. What role did your engineer play in the project? I’ve worked on similar type projects but engineer played only small role. Also you made casual reference to your cost segregation study and made a connection between the cost of the study and the difference between actual and forecast operating expenses. Can you elaborate on this comment? Thanks!

we rely on the engineers to push the project through and get all the approvals. Only if there is a zoning change, in which case the attorneys do that.

Cost segregration reports are reports that we do after completion of the construction which accelerates the depreciation. They usually cost between $8,000 and $12,000 but generate substantial deductions we would not get otherwise.

What are you seeing construction costs today running at? BTW good problem to have Sell for year 10 Proforma at Year 4 or not?

Depends on the type of project and where. On average, our cost are running around $55 to $60 psf for mostly metal buildings with all the bells and whistles. If we are doing multi story, the can run from $75 psf up. Hosever, if I really had to, without many features, I could build non-climate controlled at $35 to $40 psf.