Remember the 3 statistics we discussed last week?

- 90% of all business fail within 10 years.

- The average swing from the bottom of an economic cycle to the top is ten years.

- 90% of all business owners don’t read, or don’t know how to read a financial statement.

We are going to assume these three statistics are related. We are going to create ourselves as the 10% who succeed and create a lasting legacy using self storage as the business model.

We discussed the first of three scorecards, or financial statements, that are used to score how well we are doing in the game of business. If you didn’t watch the last episode, please do so here so this episode will be in context.

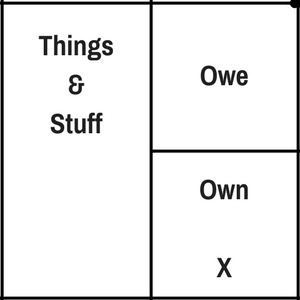

If you remember, the last scorecard, the one the scorekeepers (accountants) call a Balance Sheet, was a snapshot in time. It measured the Things & Stuff of a company. Scorekeepers call them “assets”. It also measures how much you Owe or Own. Scorekeepers call these “Liabilities” and “Equity”).

It turns out the scorekeepers say we own our profits. There are two kinds of profits reported on this scorecard. One is profits from Scorecard 2, which we’ll talk about here. The other is profits from the past that have not been paid out to the owners (called paying “dividends”). Those are “Net Revenue” or “Net Profit” and “Retained Earnings” according to the scorekeepers.

There is a lot more to this Scorecard than we discussed last week. Some we will discuss in this and other episodes and some I will most likely never talk about because I don’t know (I am a player, not a scorekeeper).

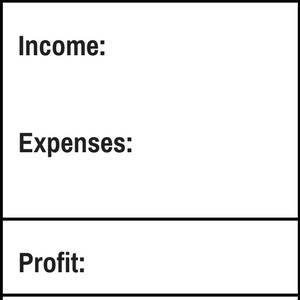

Now the second scorecard is the one everyone loves to look at.

I love to look at it.

It’s easier to understand. It seems to make sense. It looks like this:

Scorecard Two:

I looked at this for years thinking I understood what was going on. Turns out I didn’t.

Income is easy to understand, kind of. That is the amount of money coming into a company. Right? Well, kind of. In self storage it mostly is. It is the amount of money that makes it to the bank and is reported as rent, or late fees, or truck rental income.

The expenses are easy to understand, right? The cost of running a self storage project, or any business for that matter.

And if you do a good job, there is a positive number at the bottom. If we do a bad job, there is a negative number at the bottom.

Most of us who own businesses have some part of our self-worth tied up in that number at the bottom, right? Well, that is another episode to discuss that issue.

We look at that number on this scorecard, and if it is a positive number, we celebrate. If it is negative, we worry.

Don’t get me wrong. This is a critical scorecard. An important one. But it took me a long time to understand this scorecard is just a theory, not a fact.

It is the theory of “Profits” or “Net Revenue” about your company.

If you look at a monthly P & L (the scorecard for the last month) and, for example, you had $50,000 in Income and $20,000 in Expenses then in theory you made $30,000.

Now many will argue with me but think about it. Do you have $30,000 more in the bank?

Go check.

Ninety-nine time out of a hundred, you will not.

Have you ever had a great month on paper (this scorecard) and still didn’t have enough money to pay your bills?

Have you ever had a tax bill on your “Profits” and had no money to pay them.

That is because Scorecard 2 is a theory about your profits.

You can’t spend “Profits.” You can spend cash, not profits.

You see it turn out that some of the expenses have been paid, some haven’t. Most of us use “accrual accounting.” In other words, when the bills arrive they are posted. At that moment they become expenses.

Some “expenses” are paid with cash, some are paid with an IOU (a credit card for example), and some are paid next month, or in the case of property taxes, once a year. Yet, that all is listed in “Expenses” in that time period.

Some of your income may have come to you in cash. Some may have come to you in the form of an IOU (“Accounts Receivable” or “A/R”). Yet, that’s all “income” in that time period.

You see, that number we rush to look at at the bottom line is a theory. The theory about the profits your business makes. It is an important theory. For example, if this number is negative consistently, this financial scorecard is telling us our business model is not working. But this scorecard does not tell you how much cash you are making or losing. Remember, you can’t spend profits.

That is where the third scorecard comes into play. That is the “Cash Flow Statements.” What is so weird is I have never had one of the scorekeepers ever give this to me.

We will talk about that next week and tie all three together. But let’s begin to make sense of this second scorecard.

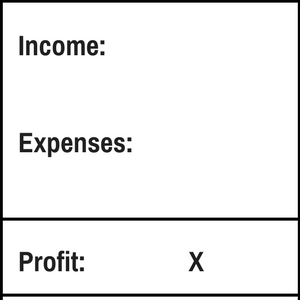

If you look at the bottom of Scorecard 2 you will see a number.

What is cool is that is the same number on Scorecard 1 in the section I call “Own.” It is called “Net Revenue” by the scorekeepers. Remember, according to them you own your profits.

Scorecard 2

Scorecard 1

Scorecard 2 is like a movie. It is the story of what happened over a time period, like March 1 through March 31. Then the number at the bottom of scorecard 2 is put on Scorecard 1 which is like a snapshot at the end of the movie.

Actions during the movie caused transactions. The transactions are turned into numbers and go on Scorecard 2.

Scorecard 2 scores the theory of profits for the company.

Scorecard 1 says here is what you have, how much cash, how much Stuff & Things, how much you owe and what are your profits. Scorecard 2 shows the theory of how it got there during a certain time period.

But if you can’t spend profits and can only spend cash, it seems like there is a scorecard missing. Right?

Well, for guys like me who are not the scorekeepers, that’s right. It’s called a “Statement of Cash Flows” by the scorekeepers. However, I have never seen one from them. I always have to go hunting it up myself.

We will talk about it next week.

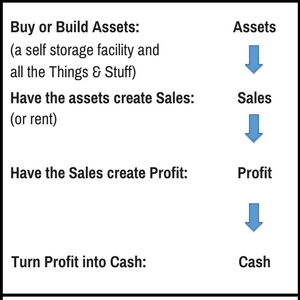

Now, remember where we started? The Things & Stuff of a company, the assets?

It could be said that the job of a business owner, you, is the following:

The real health of your company is not in how much Profit you create, but how effective you are at turning that profit into cash.

And not just any kind of cash, but a certain kind of cash.

It turns out not all cash is created equal.

Here is a preview of next week’s episode. There are three kinds of cash:

- Operating Cash

- Investment Cash

- Financing Cash.

Which cash do you think is better?

Yes, you guessed it I am sure.

We will connect all three scorecards together next week. Then you can begin to use the numbers from these scorecards to inform what to do to improve your company.